.png)

After hosting a merchant-only workshop at MPE 2026, PaymentGenes Consultancy updated its Enterprise Merchant Payment Survey with additional responses and insights gathered. The survey's main objective was to solve one of the most operationally complex decisions an enterprise merchant faces: when (and whether) to switch PSP.

Based on 58 enterprise merchants' responses, 69% of merchants with revenues above €1bn and 79% operating globally, this survey identified three key insights:

Multiple reports will be prepared in the next weeks with deep dives on different sections such as PSP migration, fraud and payment optimisation. Additionally, we will develop one-pager reports to analyse differences across different industries.

The headline finding was clear: PSP relationships at enterprise scale are under quiet but mounting pressure. However, this pressure is not translating into immediate, large-scale switching.

Instead, the market is evolving in more nuanced ways. Merchants are not abandoning providers overnight; they are building optionality. This is happening through orchestration layers, multi-acquiring strategies, and RFP processes that are often designed as much to renegotiate as to replace.

At the same time, legacy multi-PSP setups are becoming increasingly difficult to manage. More integrations, more reconciliation processes, and greater operational overhead mean that many merchants are expending significant internal resources simply to maintain the status quo.

The result is a market in transition, not through disruption, but through gradual structural change.

One of the most important insights from the survey is that merchant retention is not driven by satisfaction, but by friction.

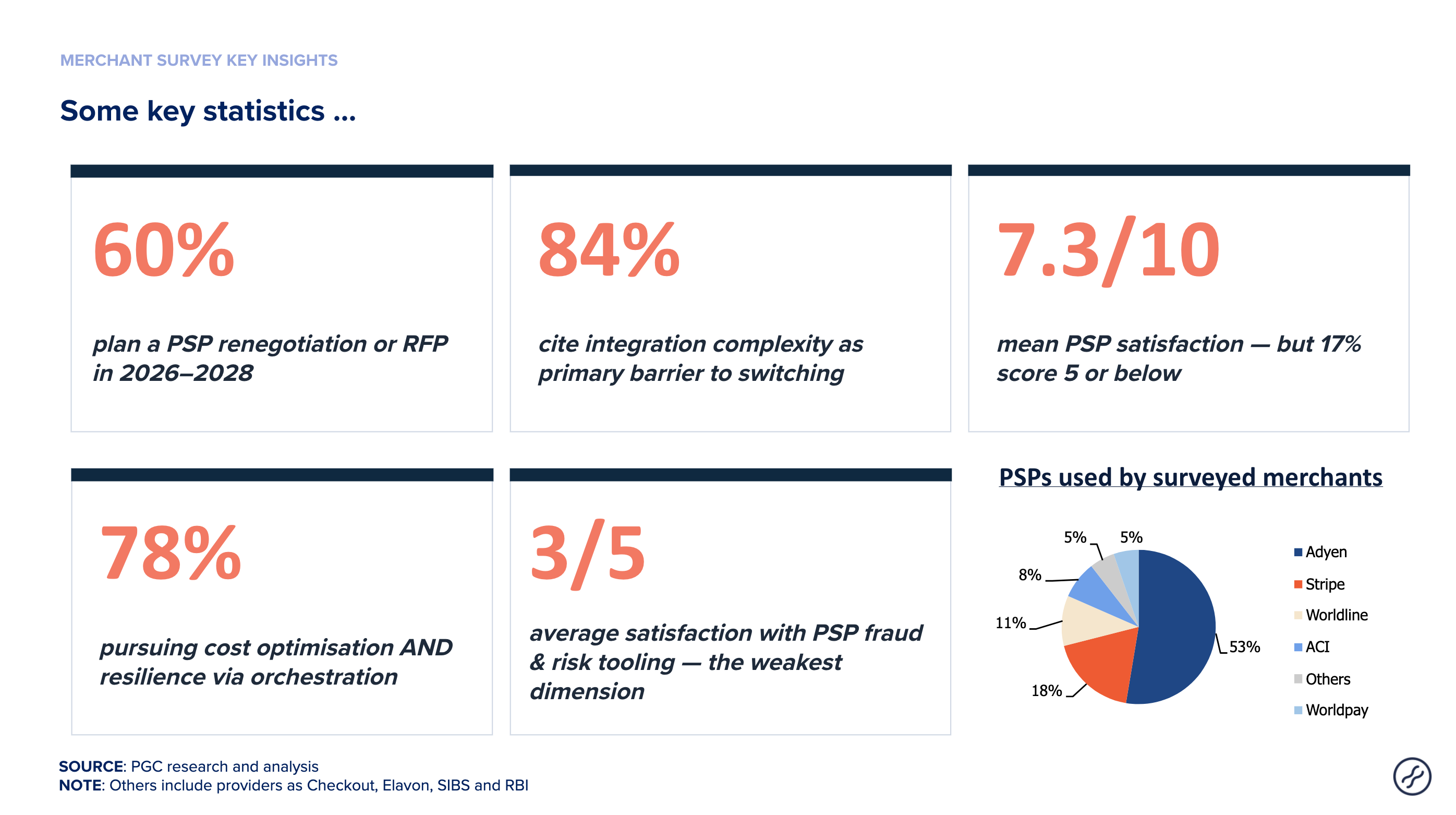

While average PSP satisfaction scores remain relatively stable (7.3/10), they mask a deeper reality: 84% of merchants are actively considering switching or at least keeping the option open.

The barriers to action are overwhelmingly operational. Integration complexity is cited by 83% of merchants, internal resourcing constraints by 66%, and contractual lock-ins by 47%. Business disruption risk — particularly around token migration and checkout stability — further reinforces this inertia.

The implication is structural: the primary moat for incumbent PSPs is not product superiority but switching friction. Any innovation that reduces migration complexity, whether technical, contractual, or operational, represents a direct threat to that moat.

“Merchants are not staying because they are satisfied, they are staying because leaving is complex.”

If inertia explains why merchants stay, commercial pressure explains when they move.

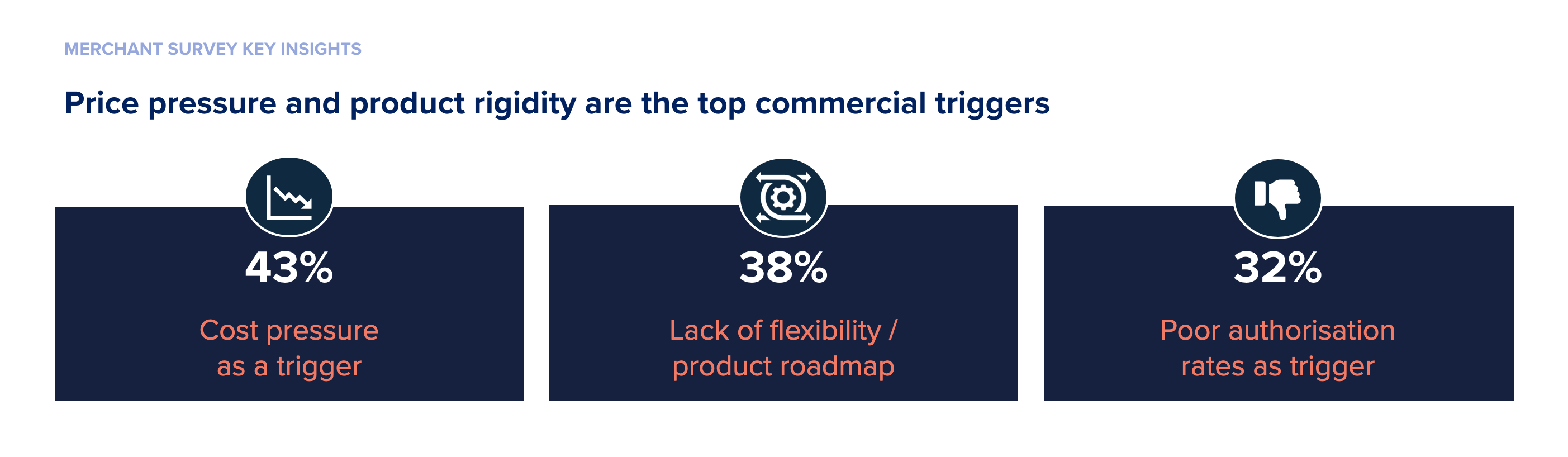

Cost remains the dominant trigger. 47% of merchants cite rising costs as the primary reason to act, making it the single most significant driver of change. Closely behind, 38% highlight their need to expand into new markets.

These are not marginal frustrations. At €1bn+ scale, merchants expect commercial leverage, tailored pricing structures, and influence over product development. When PSPs fail to evolve alongside their clients, dissatisfaction accumulates — even if it does not immediately result in switching.

Authorisation performance, lack of flexibility, and misalignment with PSP product roadmaps further compound this pressure. Even small improvements in authorisation rates can have material revenue impact, yet many merchants lack full visibility into this metric or its financial implications.

Similarly, global coverage remains a persistent gap. While 83% of merchants rank it as the most important selection criterion, delivery scores remain significantly lower, reinforcing the need for multi-PSP strategies.

Perhaps the most important structural shift highlighted in the workshop is the move away from “big bang” PSP switching towards layered architectures.

While 57% of merchants plan a renegotiation or RFP between 2026 and 2028, a full rip-and-replace remains rare. The operational risks, particularly around token migration, checkout disruption, and internal capacity, are simply too high for most organisations.

Instead, merchants are adopting orchestration layers and activating multi-acquiring strategies. Around 66% are already using or planning orchestration, enabling them to route transactions dynamically, optimise performance, and reduce dependency on any single provider.

This fundamentally changes the competitive landscape. The next wave of PSP competition is not winner-takes-all. It is about being one of several providers within a merchant’s ecosystem, and competing continuously on performance, cost, and capability.

“The next phase of PSP competition is not winner-takes-all, but continuous performance within a multi-provider setup.”

Another critical insight is that while satisfaction scores appear stable, capability gaps are widening beneath the surface.

Fraud and risk tooling, for example, consistently scores lower than other PSP capabilities, indicating that merchants increasingly rely on specialist providers or internal solutions.

At the same time, merchants are demanding more from their payment stack: better data visibility, improved reconciliation, support for local payment methods, and faster time-to-market for new regions.

This creates a growing mismatch between what PSPs deliver and what enterprise merchants require — particularly as businesses scale globally and diversify their payment mix.

Looking ahead, the payments landscape is becoming more complex, not less.

The workshop closed with a clear and pragmatic conclusion: passive waiting is no longer a viable strategy.

The question is not simply whether to stay or switch, but how to manage optionality in an increasingly complex ecosystem.

Merchants that succeed will be those that take a structured approach — understanding their cost baseline, quantifying the value of performance improvements, mapping infrastructure gaps, and defining clear triggers for action.

“Passive waiting is not a strategy; merchants are already building their exit options.”

Equally, they must decide what “good” looks like. What would a PSP need to deliver to justify a long-term relationship? And what specific trigger, a cost threshold, a market expansion gap, or a product failure, would justify initiating a switch?

These are no longer theoretical questions. They are strategic decisions that will define how merchants navigate the next phase of payments evolution.

.png)

Passporting gives PSPs the legal right to operate across the EU, but it does not guarantee operational capability, merchants must look beyond licences and verify local expertise, infrastructure, and compliance using tools like the Payments Ecosystem Directory.

.png)