.png)

Stablecoins are moving from experimentation to operationalisation. The strategic implications of this shift — and why the infrastructure layer has become critical — are explored in our latest piece.

To bring this discussion to ground level, we spoke with Bentzi Rabi, Co-founder and CEO of Utila, and Sam Eiderman, Co-founder and CTO, to understand what building this infrastructure actually requires in practice.

To bring this discussion to ground level, we spoke with Bentzi Rabi, Co-founder and CEO of Utila, and Sam Eiderman, Co-founder and CTO. Utila sits at the wallet and operations layer of the stablecoin stack: MPC-based key management, multi-chain wallet creation, policy enforcement, compliance screening, and the API layer that connects institutional backends to the blockchain.

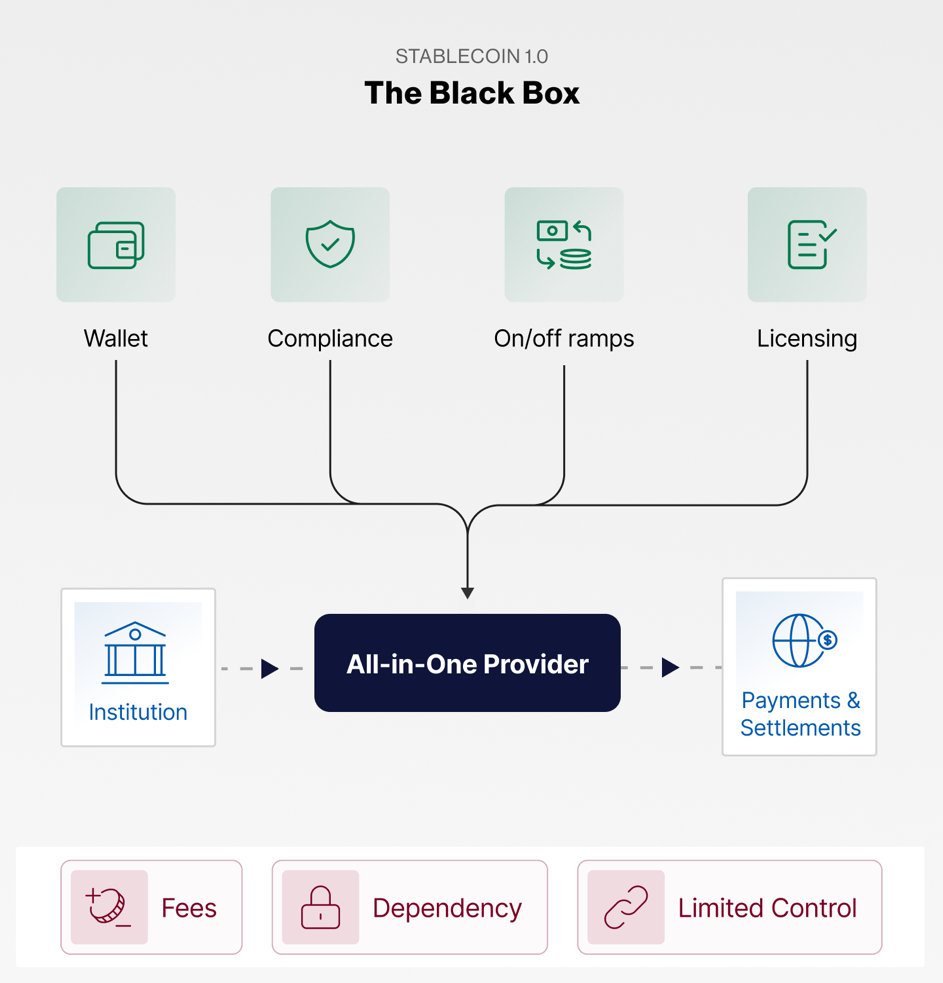

Bentzi: That a bundled provider will carry them all the way. Most organisations start their stablecoin operations with an all-in-one platform that packages wallets, compliance, on/off-ramps, and sometimes licensing into a single offering. For testing volumes and validating a use case, that makes sense. But as stablecoin volumes grow, the limitations surface: per-transaction fees that erode margins at scale, dependency on one vendor's uptime and roadmap, and limited control over compliance workflows, counterparty relationships, and governance flows. The organisations that scale successfully are the ones that plan early for infrastructure they can own and adapt.

The second misconception is that stablecoins are only a payments story. Faster settlement and lower fees across corridors are the entry point, and they're compelling. But once you have the right infrastructure in place — wallets, governance, compliance, and liquidity relationships — you can offer your clients treasury management, yield on idle balances, multi-currency settlement, and other capabilities that go well beyond a single payment rail. The full value of stablecoins only becomes accessible when the operational layer supports it. Without that infrastructure, you're limited to whatever your bundled provider has pre-packaged.

Sam: Security is the area most consistently underestimated. Companies start by choosing a key management approach — often Multisig because it's conceptually familiar — and quickly discover it doesn't hold up at institutional scale. Multisig requires chain-specific smart contracts, exposes your approval structure onchain, makes signer rotation operationally heavy, and doesn't work at all on many networks. That realisation usually pushes teams toward MPC, but selecting an MPC provider is only the beginning of the security problem.

The threat surface extends well beyond key custody. The Bybit exploit last year showed how a single compromised interface could drain $1.4 billion despite multi-party signing being in place. The Drift Protocol incident demonstrated how attackers can exploit protocol-level mechanics like Solana's durable nonces to manipulate transaction execution. To successfully mitigate these risks, multi-layered security is a must. Companies discover they need real-time threat monitoring, transaction simulation, and smart contract risk assessment on top of their wallet infrastructure. Providers like Hypernative and Blockaid offer some of these capabilities, but integrating them manually into custody and transaction workflows is meaningful engineering overhead.

Sam: It starts with a deny-by-default posture. In most traditional payment systems, transactions are permitted unless a rule blocks them. Stablecoin operations should work the other way: nothing moves unless a policy explicitly authorises it. That means every outbound transfer, every contract interaction, every token approval has to pass through a rule-based engine before it reaches the blockchain. The reason is simple — stablecoin transactions settle virtually instantaneously, and are irreversible once confirmed on-chain. There is no settlement window to intervene, no chargeback mechanism, no recall process. Controls have to work before execution or they don't work at all.

In practice, the governance layer needs to be granular and hierarchical. At the broadest level, you define which transaction types are permitted for which wallets. Below that, you set approval workflows — a CFO and COO must both sign any transfer above a certain threshold, for example. Below that, you apply specific rules: address whitelists that block transfers to unknown destinations, daily and monthly velocity limits, and policy groups that let you enforce consistent behaviour across hundreds of wallets at once.

Admin quorums — requiring multiple administrators to approve changes to the policies themselves — add another layer, ensuring that the rules governing your operations can't be quietly modified by one person.

For institutions operating in DeFi or interacting with smart contracts, governance needs to go even deeper — down to controlling which contract functions can be called, constraining input parameters, and applying rules to off-chain EIP-712 signatures so that structured messages are validated before they're authorised. These are the mechanics that prevent a single compromised interface or a social engineering attack from resulting in unauthorised fund movement.

Bentzi: Cross-border payments and B2B settlement are the two verticals with the clearest momentum. B2B stablecoin payment volume measured $226 billion last year. The driver is straightforward economics: traditional cross-border payments cost 1-2% (sometimes exceeding 3%) through correspondent banking, with multi-day settlement and limited visibility in transit. Stablecoin rails compress that to minutes (or even seconds, depending on the underlying blockchain network) at a fraction of the cost. Payment service providers serving corridors in Africa, Latin America, and Southeast Asia are moving particularly fast because they operate in regions where banking infrastructure is expensive and unreliable, and stablecoins offer a credible alternative.

The second area accelerating is internal treasury and global money movement. Companies with entities and bank accounts across geographies are using stablecoins to replace multi-hop correspondent banking for intercompany transfers. A transfer from Germany to Brazil that takes a week through traditional rails settles in seconds or minutes on stablecoin infrastructure, with full visibility and programmatic controls.

The gains in capital efficiency that this entails cannot be overstated. Companies can reduce idle cash buffers maintained at each location to cover settlement delays. And now that regulatory clarity from MiCA in Europe and the GENIUS Act in the US has made institutional treasury teams more comfortable putting stablecoins into production workflows, we will only see more companies wake up to these opportunities.

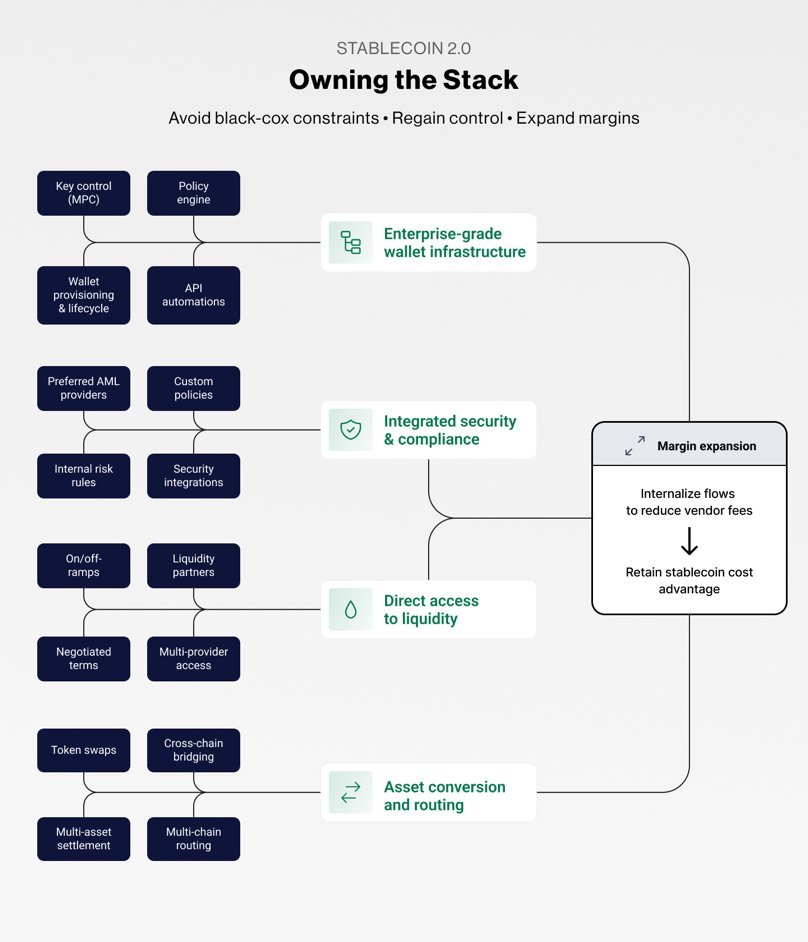

Bentzi: The decision should start with the question of what you need to control to protect your margins and serve your customers, versus what parts of the infrastructure you can consume through a partner because they are undifferentiated.

For most mid-sized PSPs and fintechs, four elements sit at the control boundary: wallet infrastructure (because it determines how you attribute funds, segregate client assets, and manage keys), compliance integration (because your regulatory obligations are yours regardless of who runs the screening), liquidity access (because your on/off-ramp relationships directly affect your unit economics), and asset conversion and routing (because your counterparties will not all use the same stablecoin on the same chain).

What you should not build is the cryptographic layer beneath those capabilities. MPC key management, multi-chain transaction signing, gas abstraction, and the API and webhook infrastructure that connects your backend to the blockchain are deep platform engineering problems. Building them in-house means hiring specialized cryptography and blockchain teams, maintaining that infrastructure across every chain your customers need, and keeping pace with an evolving security landscape.

The practical path for most mid-sized operators is to own the operational layer — your wallets, your compliance vendor, your ramp relationships, your policies — while running it on infrastructure purpose-built for that job. That way each step toward full independence is a configuration change, not a migration.

Bentzi: The most significant shift will be from siloed vertical solutions to composable infrastructure stacks. Over the next two to three years, we expect the market to move toward modular architectures where institutions own their core infrastructure — wallet layer, policy engine, compliance integrations — and connect to specialized providers for liquidity, fiat connectivity, and yield through standardized interfaces.

The second evolution is in connectivity. As more institutions operate on stablecoin rails, counterparty discovery and settlement become critical infrastructure. Today, establishing a new ramp provider or liquidity relationship involves manual onboarding, address whitelisting, and operational setup. Network layers that let institutions discover verified counterparties, negotiate terms, and settle directly — without rebuilding their compliance and wallet setup for each new relationship — will become a core part of the stack.

Yield on idle stablecoin balances will also mature as an institutional product category, with regulated and permissionless options available through the same infrastructure that handles payments and treasury. The infrastructure providers that survive will be the ones whose platform can support payments, treasury, settlement, and yield as different configurations of the same underlying capabilities.

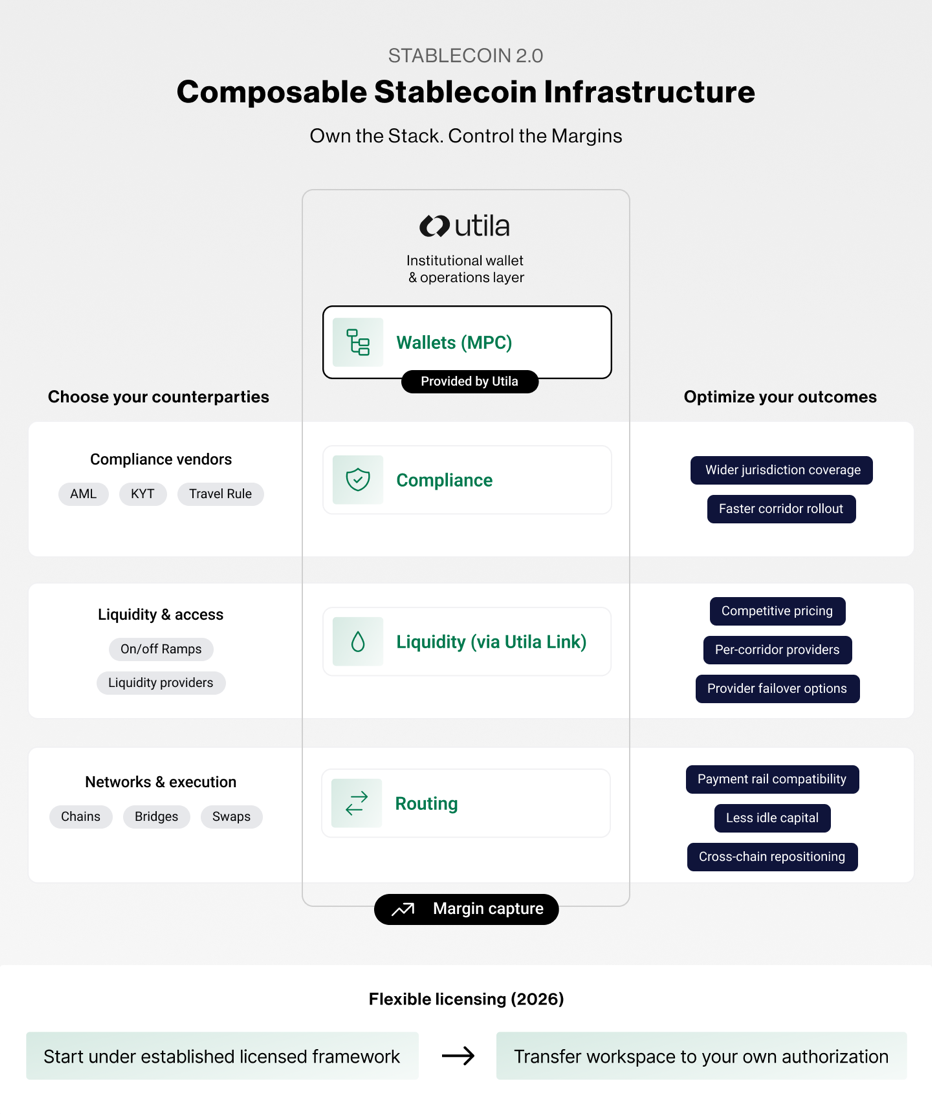

Bentzi: Utila sits at the wallet and operations layer of the stablecoin stack. We provide the infrastructure that institutions use to store, move, and govern digital assets — MPC-based key management, multi-chain wallet creation, policy enforcement, compliance screening, gas management, and the API layer that connects all of it to the institution's backend systems.

Our core control point is the intersection of custody and governance. Whoever controls the keys and the policies around those keys controls the operational stack. In Utila's architecture, the institution retains direct control of its keys through a self-custodial MPC model — one key shard is held by the institution, one by Utila, and neither party can move funds alone.

The policy engine then governs every action: who can initiate transfers, who must approve them, what limits apply, and which compliance checks run before execution. That combination — secure key management plus enforceable governance — is what makes stablecoins usable in regulated, production environments. Everything else in the stack depends on it.

Bentzi: Basic wallet creation and transaction signing are commoditizing. The differentiation is in the operational layer above it: how granularly you can define and enforce policies across wallets, how deeply compliance is embedded in the transaction flow, how flexibly you can connect to different ramp and liquidity providers without re-platforming, and how well the API and automation layer integrates with the institution's existing systems. An institution running thousands of wallets across multiple chains with different compliance requirements per jurisdiction and multi-step approval workflows for different transaction types needs a platform that can handle that configuration complexity reliably.

The other axis of differentiation is architectural openness. Bundled providers that lock institutions into a specific AML vendor, a specific ramp partner, or a specific set of supported chains create the same dependency problems that institutions are trying to escape by moving to stablecoins in the first place.

Infrastructure that lets you choose your compliance provider, negotiate directly with your ramp partners, add chains as your business requires, and eventually transition from operating under a partner's license to your own authorization — without migrating your stack — compounds in value as the institution scales. The providers that treat vendor lock-in as a feature will lose share to the ones that treat modularity as a design principle.

Sam: The capability to get it right is governance and key control. Before anything else — before selecting ramp partners, before deciding which chains to support, before launching a product — the institution needs to establish how private keys are managed, who can authorise transactions, and how policies are enforced. If you get this wrong, every other decision inherits that weakness.

The capability most often overestimated is chain selection. Many organisations devote disproportionate attention to deciding which blockchains to support, treating it as a major strategic commitment. In practice, multi-chain support is a solvable infrastructure problem - a well-designed wallet platform lets you add networks as your counterparties and corridors require them, without re-architecting your stack. The more consequential decisions - wallet architecture, compliance workflow design, policy configuration, and the build-versus-partner strategy for the operational stack - receive less attention because they are less technically visible, even though they have a larger impact on long-term cost structure, regulatory readiness, and operational resilience.

Bentzi: The question facing payments executives today is not whether stablecoins work as a settlement layer. The transaction volumes, the regulatory frameworks, and the institutional adoption patterns have already answered that. The real question is whether your organisation can operate on these rails with the same level of control, compliance, and operational discipline you apply to traditional payment infrastructure. That is an infrastructure problem, and it requires infrastructure decisions.

The organisations that will capture the most value from this shift are the ones that invest in owning the operational layer. Starting with a bundled provider is a reasonable first step, but the strategic imperative is to build toward a stack you control — where adding a new corridor, switching a ramp partner, or responding to a regulatory change is a configuration adjustment, not a vendor negotiation. The margin, resilience, and flexibility advantages of that approach compound with every dollar of volume that moves through the system.

The conversation with Utila reinforces what at PaymentGenes we observe across the fintech and financial services market. The organisations that will lead in payments over the next three to five years are not necessarily the ones with the most innovative products — they are the ones that get the infrastructure layer right at the right moment. That window is open now, and it will not stay open indefinitely.

To help you navigate this, we want to share three questions we would put to any Head of Strategy or C-level leader in payments right now:

Stablecoins have crossed the threshold. They are no longer a crypto story, a niche use case, or a regulatory question mark. They are emerging core payments infrastructure, and the operational challenge has shifted accordingly.

The organisations that will capture the most value from this shift are not necessarily the first to launch a stablecoin product. They are the ones that build — or acquire — the operational foundation that makes scale possible: controlled key management, enforceable governance, embedded compliance, and the flexibility to add corridors, chains, and counterparty relationships without re-platforming.

That foundation is available today. The question for every payments executive reading this is a simple one: is it on your agenda?

Secure Stablecoin & Digital Asset Infrastructure for Fintechs and Enterprises

Utila provides fintechs, PSPs, banks, and enterprises with institutional-grade infrastructure to build and manage stablecoin and digital asset operations at scale. The platform covers the full operational stack:

Utila is SOC 2 Type II compliant, supports 100+ blockchains, and connects to 30+ ecosystem partners, including exchanges, on/off-ramps, AML/KYT providers, and yield venues. Most teams are on board in under five minutes.

Ready to explore what stablecoin infrastructure looks like for your organisation?

Visit utila.io to speak with the team.

PaymentGenes Consultancy is a boutique strategy and M&A advisory firm focused exclusively on the fintech and payments sector. We advise fintechs, PSPs, banks, and investors on market entry, strategic partnerships, and transactions.

PaymentGenes Consultancy is a boutique strategy and M&A advisory firm focused exclusively on the fintech and payments sector. We advise fintechs, PSPs, banks, and investors on market entry, strategic partnerships, and transactions.

.png)

.png)

.png)