Hosted by Ward Hagenaar and Bas van Donselaar, the Digital Euro Round Table at MPE 2026 tackled one of the most consequential questions facing the payments industry today: is the ecosystem actually ready for the Digital Euro, and does the current design make sense?

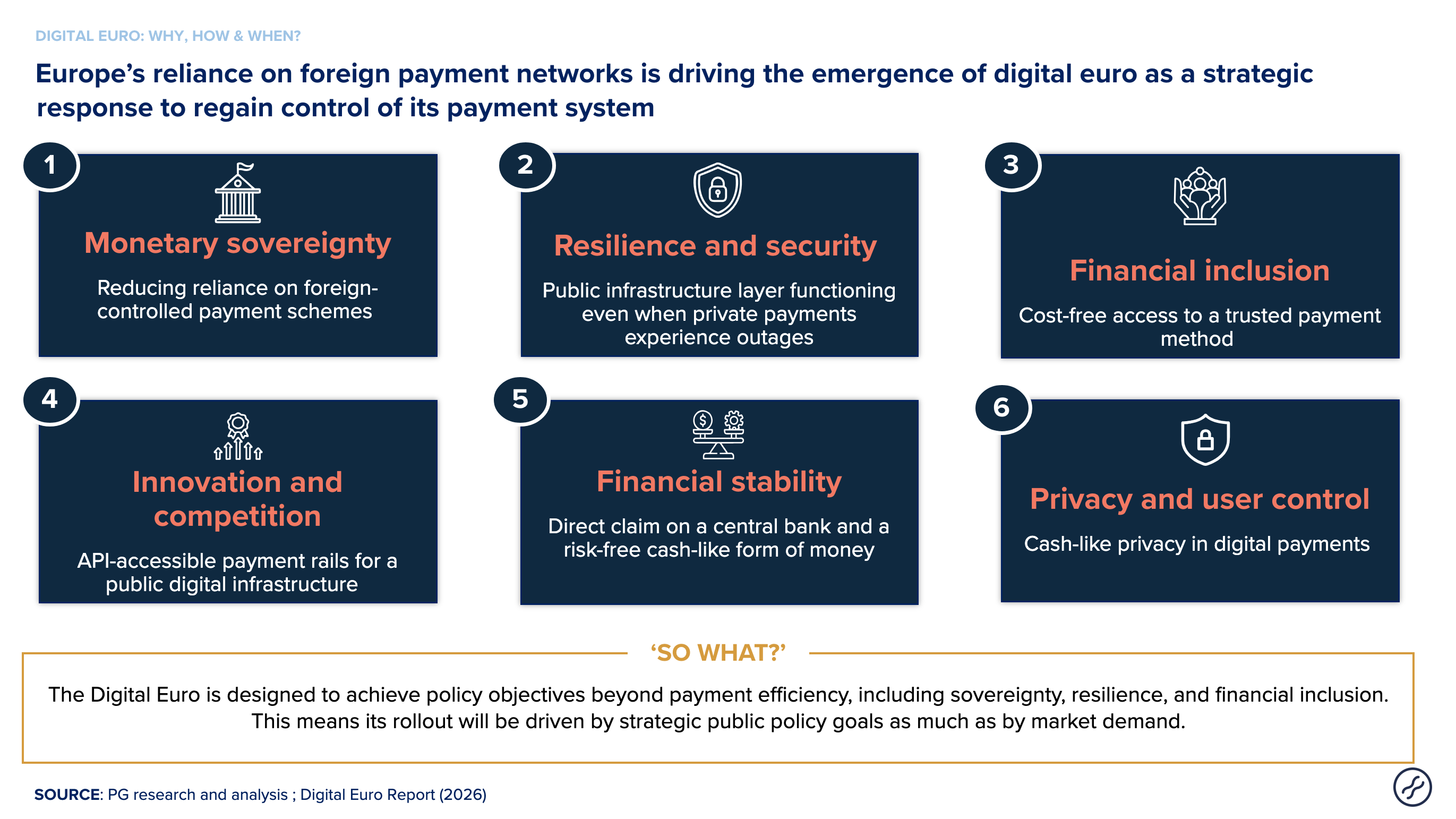

The session opened with the fundamental question of why the Digital Euro exists at all. Europe's growing reliance on foreign-controlled payment networks has made monetary sovereignty a strategic priority. The Digital Euro is the ECB's response, a state-backed, privacy-by-design payment instrument designed to preserve public money in a digital economy, strengthen European payments sovereignty, and provide cost-free financial inclusion at scale.

But ambition and readiness are two different things.

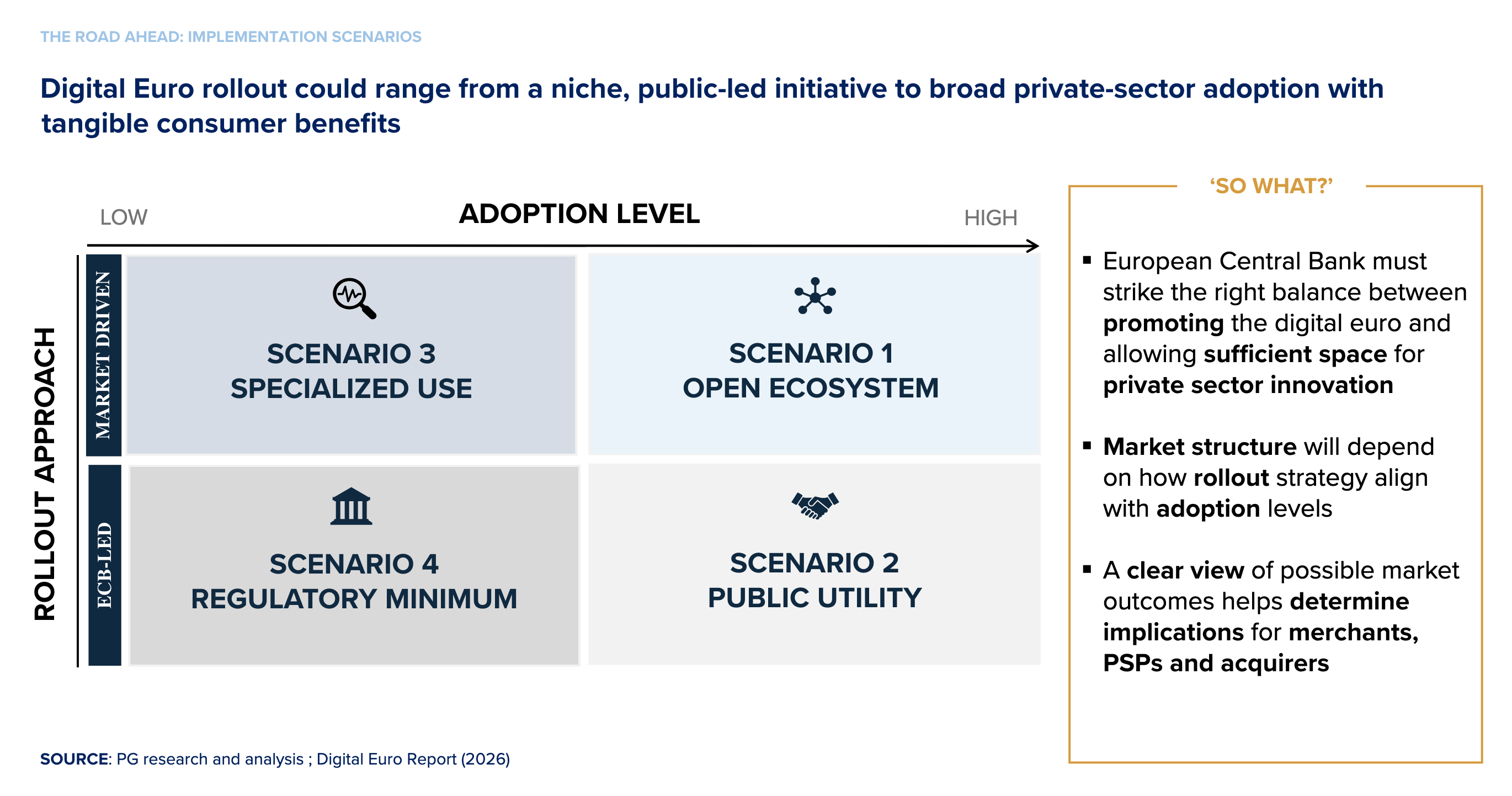

The roundtable explored four possible rollout scenarios, ranging from an Open Ecosystem driven by broad private-sector adoption to a Regulatory Minimum where compliance costs arrive without meaningful transaction volumes. The difference between these outcomes matters enormously. For merchants, a credible Digital Euro rail could provide real negotiating leverage against card schemes and lower acceptance costs. A poorly adopted mandate, on the other hand, means integration costs with no economic upside.

For PSPs, the stakes are equally high. Whoever owns the wallet layer controls the consumer relationship. For acquirers, the risk is margin compression as processing shifts toward utility-style infrastructure economics.

What emerged clearly from the discussion is that the confirmed ECB policies, universal access, privacy by design, mandatory acceptance thresholds, merchant fee caps, are a foundation, not a final blueprint. Key implementation details remain open, and

the organisations that engage now will have a direct influence on how those details are resolved.

One of the central tensions highlighted in the workshop is that the Digital Euro is not purely a market-driven innovation. It is a policy-led initiative designed to achieve broader objectives: sovereignty, resilience, financial inclusion, and systemic stability.

This distinction matters. Unlike cards or wallets that succeed based on user demand and commercial incentives, the Digital Euro will likely be pushed forward regardless of immediate adoption. As a result, its success depends on aligning three forces: public policy ambition, private-sector incentives, and consumer behaviour.

The challenge is that these forces are not naturally aligned. Stakeholder perspectives remain fragmented. Central banks are strongly committed to the initiative, while commercial banks remain cautious due to disintermediation risks. PSPs and fintechs see opportunity but require open infrastructure to innovate. Merchants are pragmatic, focusing primarily on cost, adoption, and customer experience at checkout.

This fragmentation reinforces a key point: the final shape of the Digital Euro will be the result of trade-offs, not a perfectly optimised system.

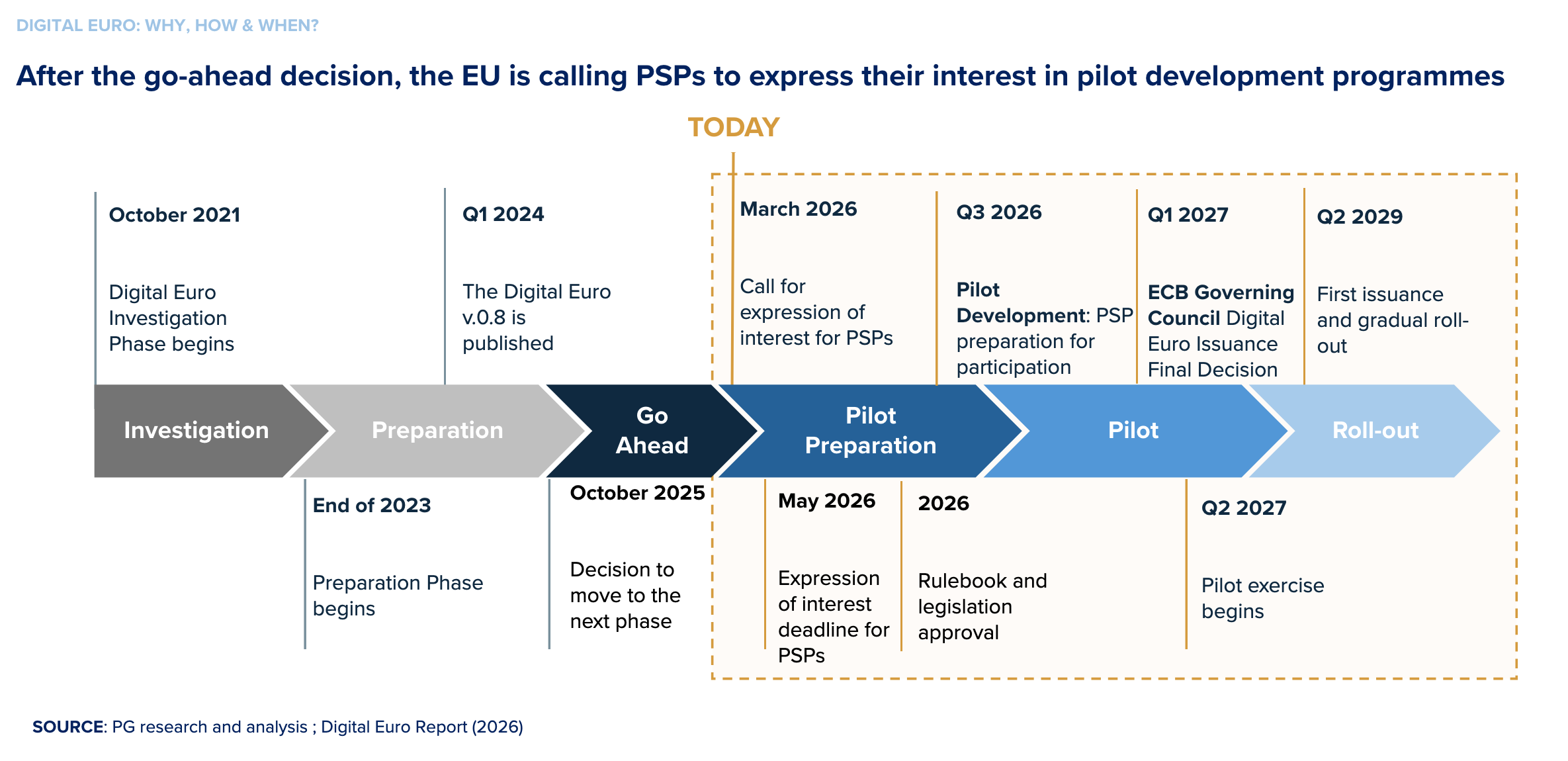

Another critical insight from the session is timing. The initiative has already moved beyond the conceptual phase. The ECB has taken its go-ahead decision, and the legislative process is well underway, though it is ultimately legislation, not the ECB alone, that will determine the final shape and pace of the rollout. Pilot programmes are expected around 2027, with a potential first issuance from 2029 onwards. The window to engage and influence the outcome is narrower than many organisations realise.

Importantly, participation in early pilots is not cost-neutral. PSPs and other players must invest upfront without immediate financial return. Those involved in pilots and rulebook development will help shape technical standards, access rules, and commercial frameworks.

This creates a strategic asymmetry. Players that engage early can shape the system. Those that wait will have to adapt to it.

The importance of rollout scenarios

The session mapping four possible rollout scenarios and assessing their impact on each player in the payments chain.

The four scenarios are defined by two axes: how market-driven versus ECB-led the rollout is, and how high or low consumer adoption turns out to be.

The key implication cutting across all four scenarios is this: meaningful upside only materialises if the Digital Euro becomes a genuinely competitive payment rail. Central bank rollout alone will not shift competition without broad private-sector uptake, and limited adoption risks confining it to niche public infrastructure rather than a widely used payment method.

Crucially, the difference between these scenarios is not driven by technology, but by incentives. Consumer value propositions, PSP business models, and regulatory calibration will ultimately determine whether the Digital Euro scales or stagnates.

For merchants, the opportunity lies in cost leverage and diversification of payment rails. If the Digital Euro reaches scale, it could reduce dependency on card schemes and improve negotiating power. It also introduces new functional possibilities, particularly through conditional payments and programmable settlement flows.

For PSPs, the battleground shifts to the wallet layer. If PSPs can position themselves as the primary interface for Digital Euro usage, they retain control over the customer relationship and can build value-added services on top. If not, there is a real risk that payments become commoditized infrastructure, with value shifting toward wallet providers or BigTech players.

For acquirers, the outlook is structurally challenging. While they are likely to remain embedded in the acceptance flow, large-scale Digital Euro adoption could compress margins by reducing scheme-based economics and pushing pricing toward utility levels.

Across all stakeholders, one theme is consistent: the Digital Euro redistributes value rather than simply creating new value.

The session closed with a pragmatic framework: five no-regret investments that apply regardless of which scenario materialises.

The Digital Euro is not a binary outcome. It is a spectrum of possible futures shaped by policy decisions, market dynamics, and strategic choices made today.

For now, the key takeaway is not whether the Digital Euro will happen, but how it will happen, and who will shape it.

.png)

.png)

.png)